On July 18th SAP released their 2nd quarter 2013 results - you can see the results here and listen to the recording here.

Cloud and HANA saved SAP's Q2 - almost

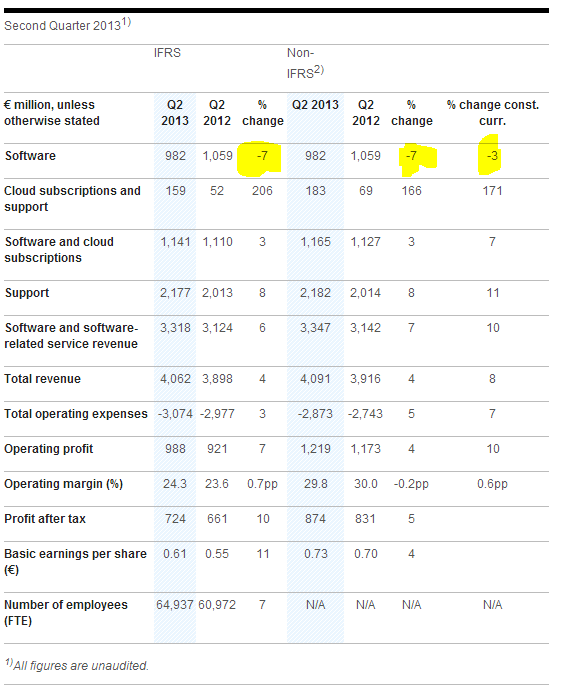

For the first time in a long time, SAP did not grow their software license revenue. In Q2, SAP recorded 982ME in license revenue, which is down 77M E less that quarter Year over Year. Instead of addressing the drop in new license growth, SAP emphasizes the overall growth of its software and cloud subscriptions revenue, a paltry 3% or 1.141ME.

Of the 982ME, in the overall software number, 102ME HANA revenue is included. Should we remove HANA - only 880ME would have been recorded in Q2 2013. In Q2 2012 SAP recorded 85 ME HANA revenue - bringing SAP's Q2 software number to 974 ME.

Consequently, it looks like the SAP core business is down by a ballpark of 10+%.

|

| From SAP website. |

The cloud subscriptions and support revenue grew from 52 to 159ME, a 206% increase, which is good news - at first glance.

But let's dissect the cloud subscriptions and support revenue a little further. This is revenue that comes from SAP home built SaaS applications (like byDesign or the SaaS CRM product) - but mainly from the former Successfactors and Ariba products. If we do a ceteris paribus and assume that the revenues of Successfactors and Ariba would remain constant - not withstanding the SAP acquisition - then these should contribute 76.6 MUS$ (Ariba) and Successfactors claimed 73.2 MUS$ - which is a total of - let's round up - 150 MUS$ - at today's exchange rate 107 ME (all based on calendar Q2 2011 data - as 2012 they were already acquired / being acquired). So the good news is, that there is growth in these numbers and SAP's homegrown SaaS products must be contributing - but not the stellar growth rate that SAP wants us to believe in.

Why is SAP weak in core license sale?

The questions from the financial analysts unfortunately did not point into this area - so we can only speculate - and state to what we know.

SAP is well licensed if not over licensed for most of their accounts in North America and Europe. So SAP needs to sell the business suite where it's not yet in the market and there it is focusing on the BRIC countries - and it seems to have done a very good job in Brazil. And it singled Mexiko out as well. But SAP - like all vendors - seems to have had issues in APAC. Basically SAP needs to execute very well in the BRIC countries to keep up core license sales, if these markets do not do well economically or if SAP blunders execution - then SAP won't be able to keep up core license sales. If HANA would not be around - SAP would be a shrinking company on the license revenue side.

And HANA is the product that SAP need to fill the missing revenue - but it looks like SAP was asking for too much from the just two year old in Q2 - as HANA revenues grew only by 20%. SAP said that HANA deals are year end loaded - which leads to the impression that SAP and their sales reps are using HANA to close the year well in Q4. Any missing sales could be filled with HANA licenses for running the Suite on it - starting a push in the fall. Always assuming customers have budget and SAP can convince them of a winning value proposition to move the Suite on HANA.

If SAP is a cloud company...

Through the conference call both Bill McDermott and Jim Hagemann-Snabe referred multiple times to their view that the cloud age has started, customers are buying cloud products etc. - they should have been asked then, how they plan to convert their product portfolio from a mixed portfolio to a more and more cloud based product portfolio.

We all know, that SAP has a number of homegrown SaaS products and then the acquired entities like Successfactors, Ariba and hybris. But this is not a complete SaaS suite - so either SAP is missing out on bringing all its products to the cloud - or it's only a partial push to SaaS. This will be a vital area to watch as SAP does not have any SaaS offerings in Finance and Manufacturing, two key enterprise automation areas.

Verticals to the rescue?

SAP seems to have gotten more focus on their vertical offerings recently. Certainly making Verticals Hagemann-Snabe main responsibility has helped the matter. And certainly SAP has significantly more potential on the vertical side than for its horizontal offering. Overall the market has been under penetrated and mostly been addressed with customization. But with the main focus being to move Suite customers on HANA - it may be tough to convince customers, who are not on HANA to move to an industry offering that may be improved or upgraded soon. SAP will need to explain how vertical investments can be used between the older conventional database platforms and the new HANA platform.

The larger challenge is that in the past SAP - like other enterprise automation vendors - has not been able to solve the vertical automation puzzle yet, for a variety of reasons (good for a whole other blog post). But that does not mean that SAP may not be able to address and solve this now for the first time. Assuming SAP will succeed - this will however not address the overall revenue challenge that SAP faces. The reason is that in most sales scenarios the vertical functionality is an add-on from a revenue portion - compared to the horizontal piece of the pie. And true - there is untapped potential - those enterprises that have not been conquered by standard software vendors yet - banking anyone? But these opportunities form the minority of the overall vertical enterprise automation market - so at the end of the day, even a very successful execution by SAP on the vertical opportunity - will only be able to address a smaller portion of the SAP revenue challenge that SAP faces.

Can the sales force do it?

SAP has a formidable sales force - but it's an on premise enterprise application license sales force. Traditionally SAP succeeded to sell the integrated suite vision to the executives to who the overall working of the enterprises matters - to the CEO, CFO and CIO. But SaaS applications are often sold to the line of business executive - often against the establishment guidelines and standards. Sales reps need to setup a whole new set of relationships - that are even harder to develop since they sold SAP to these companies before - and that wasn't always a popular decision with the line of business executives. Many, many preferred products and installations that were used and preferred in a division or line of business - got replaced by SAP as the central, CxO mandated product. It's not only hard to change the comfort zone - but the SAP sales reps also need to re-invent themselves.

The other challenge we see for the salesforce is, that they are an enterprise application sales force that now needs to sell HANA technology. And while it should be still easy for an applications sales rep to sell the move from another database to HANA - after all SAP was always sold with a database - it's a different story to sell pure HANA technology opportunities. SAP recently told me - correctly - that of course SAP still has sales reps selling Sybase - but that salesforce does not have the reach and cannot generate the volume that SAP needs from HANA - which is around at least 1 BE in the next 4 quarters.

So it's good news for the salesforce when we learnt - deep buried in the Q&A section of the earnings call - that SAP has made the sales of on premise vs on cloud commission neutral to the sales reps, which used to be one of the primary challenges of vendors transitioning from license to service products. But SAP will have to do a lot to re-train or hire a technology sales force that can sell north of 1 BE of HANA licenses year after year.

The reason is that enterprise application sales reps are a different breed of sales reps than the enterprise technology sales reps. While an application sales rep is supposed to sell the standard automation as much as possible that is supported in the product - the technology sales rep is supposed to chase non standard automation, that can be built on the technology's standard capabilities. Both skills are seldom combined in professionals, who even if they have them - need to build separate relationships and rapports with their customers and prospects.

MyPOV

We are seeing some potential structural revenue challenges coming up on SAP's horizon. Emerging markets and HANA may not be enough revenue potential that SAP can exploit, to keep traditional license revenue growing. And SAP will need to have a lot of help from the new subscription based services to compensate for the reduced core license revenue. Or monetize other markets like mobile and social better.

We will see how the SAP co-CEOs will address this challenge going forward and wish them luck on the journey - as a strong and growing SAP is better for the market place and its customers

And lastly I would have hoped my fellow financial analyst colleagues would have harped more on these questions in the Q&A section - but what hasn't happened - can still happen.